Buffett knows that his letters are long, and partner had difficulty to read entire letters, so he point out few points, he called it’s a “Ground Rules”

Following are the ground rules, please go through it, and the message behind the rules never change, like rule no 1 says no returns are guaranteed to partner, it’s not for partner alone, in equity investment, returns are not guaranteed, let’s see the Ground Rules.

1. In no sense is any rate of return guaranteed to partners. Partners who withdraw one-half of 1% monthly are doing just that–withdrawing. If we earn more than 6% per annum over a period of years, the withdrawals will be covered by earnings and the principal will increase. If we don’t earn 6%, the monthly payments are partially or wholly a return of capital.

2. Any year in which we fail to achieve at least a plus 6% performance will be followed by a year when partners receiving monthly payments will find those payments lowered.

3. Whenever we talk of yearly gains or losses, we are talking about market values; that is, how we stand with assets valued at market at yearend against how we stood on the same basis at the beginning of the year. This may bear very little relationship to the realized results for tax purposes in a given year.

4. Whether we do a good job or a poor job is not to be measured by whether we are plus or minus for the year. It is instead to be measured against the general experience in securities as measured by the Dow- Jones Industrial Average, leading investment companies, etc. If our record is better than that of these yardsticks, we consider it a good year whether we are plus or minus. If we do poorer, we deserve the tomatoes.

5. While I much prefer a five-year test, I feel three years is an absolute minimum for judging performance. It is a certainty that we will have years when the partnership performance is poorer, perhaps substantially so, than the Dow. If any three-year or longer period produces poor results, we all should start looking around for other places to have our money. An exception to the latter statement would be three years covering a speculative explosion in a bull market.

6. I am not in the business of predicting general stock market or business fluctuations. If you think I can do this, or think it is essential to an investment program, you should not be in the partnership.

7. I cannot promise results to partners. What I can and do promise is that:

a. Our investments will be chosen on the basis of value, not popularity;

b. That we will attempt to bring risk of permanent capital loss (not short-term quotational loss) to an absolute minimum by obtaining a wide margin of safety in each commitment and a diversity of commitments; and

c. My wife, children and I will have virtually our entire net worth invested in the partnership.

Each and every point, has a great message, point number seven was the promise of Buffett to partners, Investment chosen on the basis of value, avoid permanent loss of capital by buying on huge margin of safety, and last one, Buffett has entire net worth invested in partnership, (Skin In the Game)

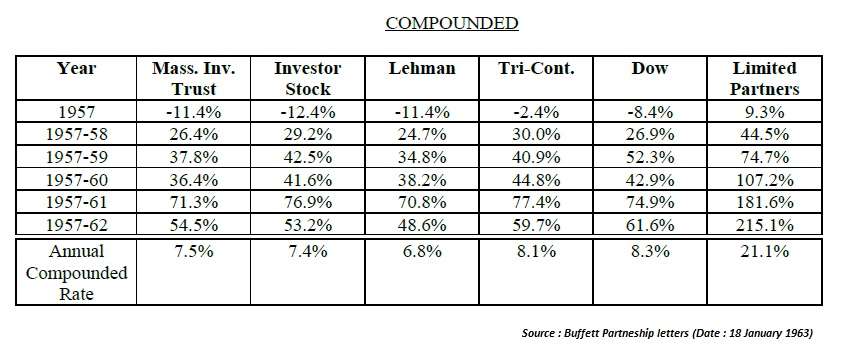

Our Performance in 1962

Due to string rally in the last few months, The Dow did not have any significant decline,

Lot of action over the entire period, The general public, is jot too far from where it was in 1959 or 1960. If any investor had invested in last year had a negative return of -10.8% if dividend included the figure comes -7.6%, where as Buffett partners return was +13.9%

The following table shows the combine results of all partners, and the annual rate of compounding, and average annual rate of compounding over the entire period.

After reading above data, partners expect the same results over the coming years, so Buffett writes…

My (unscientific) opinion is that a margin of ten percentage points per annum over the Dow is the very maximum that can be achieved with invested funds over any long period of years, so it may be well to mentally modify some of the above figures.

Buffett expects 10% point margin over the Dow, but don’t expect above results, and be mentally ready to modify the above figure. Buffett always thinks, what his partners might think,

It’s a classic case of Hindsight Bias, Sometimes called the “I-knew-it-all-along” effect, the tendency to see past events as being predictable at the time those events happened. (Source: Wikipedia) avoid hindsight bias at all cost, history repeat itself, but not the same as always. This bias, you can find everywhere, from everyday decision making to long term decision making.

Partners have concerns about the size of the funds, as Buffett writes, situations where larger sums helped, and some where it has hindered.

Investment Companies

As Buffett, benchmark his return against Dow as well as two open ended and two closed ended mutual funds, the results as follows,

Following are the compounded returns of all four mutual funds and Dow compounded rates over the same period of time, as Limited partners results shine out, its due to buying companies, at very large margin of safety, avoid popular investment, and insulate portfolio by investing in special situations (workouts)

Buffett Compounding rate was 21.1% where all mutual fund and Dow lags.

The Joys Of Compounding

As Buffett write about the example of Columbus, who underwrote the Voyage Isabella for $30000, without attempt to evaluating the monetary benefits.

On the other hands if $30000 invested at 4% compounded annually would have amounted to $2,000,000,000,000 that’s $2 trillion.

Compounding happens due to long period of time and the rate of compounding.

The above table shows the $100000 compounded at 5%, 10% and 15% for 10, 20 and 30 years. The important point to note is that relatively small difference in rates, yields great sums over a long period of time.

If Investors, like to have a great returns, the few percentage points advantage over the Dow is great, don’t look for extraordinary returns every year, look for companies, who give decent returns over long period of time, that’s why Buffett looks for companies having Durable Competitive Advantage i.e. MOAT, only those companies, sustain the profitability and increase ROE,

Buffett famously says…

“Time is the friend of the wonderful business, and enemy of mediocre business”

Our Method of Operation

In this section, Buffett write about the style he used for investment operations.

There are three methods

1) Generals: Undervalued securities, nothing to say about corporate policies

2) Work-outs: Whose financial results depend upon corporate actions.

3) Control: Where Buffett take large position and attempt to influence policies of the company

You can read more about these three methods in 1961 letter Click here

Dempster Mill Manufacturing Company

Buffett has 73% of portfolio holding in Dempster Mill, the company’s main business is in farm equipment, water systems, water well supplies and plumbing lines.

The problem with Dempster was the sales of the company was not growing, low inventory level and no profits in invested capital, it’s a classic case of value trap, where you get a value in stock purchase in relation to price, but the business itself is bad, or management is not capable to turnaround the business.

Buffett bought this company in August 1961 at an average price of $28 per share, having bought few stocks at $16, but majority of purchase was done at $30.25 per share. Buffett take control of the company, and he was not bothered about the general stock price, he bothered about the value of assets.

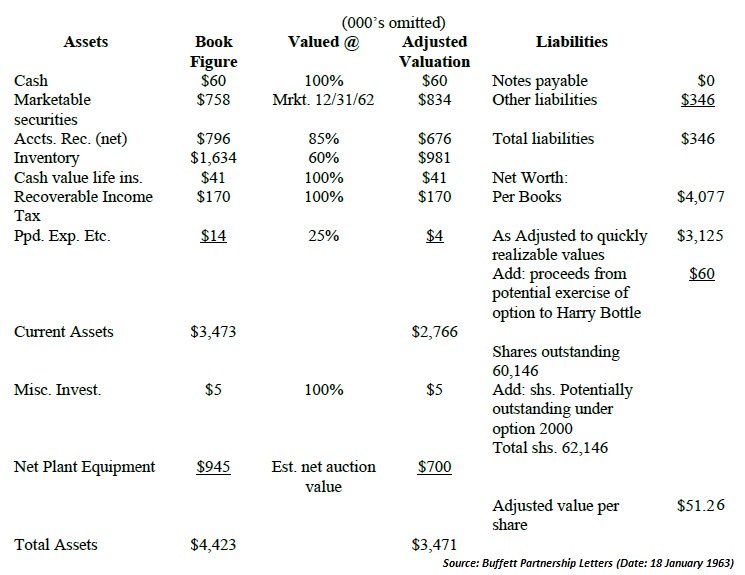

The above picture is the consolidated balance sheet of Dempster Mill, Buffett use appropriate discounts to the various assets, these valuation based on their non earning assets and not access on the basis of potential, but on the basis of what Buffett thought sales would produce on that date. Buffett thinks the fair value of the Business is at $35.25 per share.

As cash valued at 100%, Account receivable valued at 85%, Inventory Valued at 60%, Ppd Exp valued at 25%, Cash valued at 100%, finally the value per share determined at $35.25.

Dempster financial year ends at November 30th. Value per share was $35.

Initially Buffett works with the old management, for effective use of capital, better margin, reduction of overhead, these efforts were fruitless, after six months, it becomes obvious that old management not committed and they were unwilling towards Buffett’s objective. Buffett looks for the change in management.

Harry Bottle, comes in picture, to solve the problem of Dempster mills. Buffett meet Harry in Los Angeles on 17 April 1962, Buffett presented a deal which provide rewards based on objective achievement. 23 April he was appointed as president of the company.

Harry is unquestionably the man of the year. Every goal we have set for Harry has been met, and all the surprises have been on the pleasant side. He has accomplished one thing after another that has been labelled as impossible, and has always taken the tough things first. Our breakeven point has been cut virtually in half, slow moving or dead merchandise has been sold or written off, marketing procedures have been revamped, and unprofitable facilities have been sold.

The results of this program are partially shown in the balance sheet below, which, since it still represents nonearning assets, is valued on the same basis as last year.

Harry Bottle done a great job, as Buffett points out three facts,

1) Net worth reduce, by writedowns of Inventory, Fixed Assets by $550000, Converted assets to cash

2) Converted Assets of manufacturing business (which has been a poor business) to a business which we think is a good business –securities. Buffett bought more securities by selling the assets.

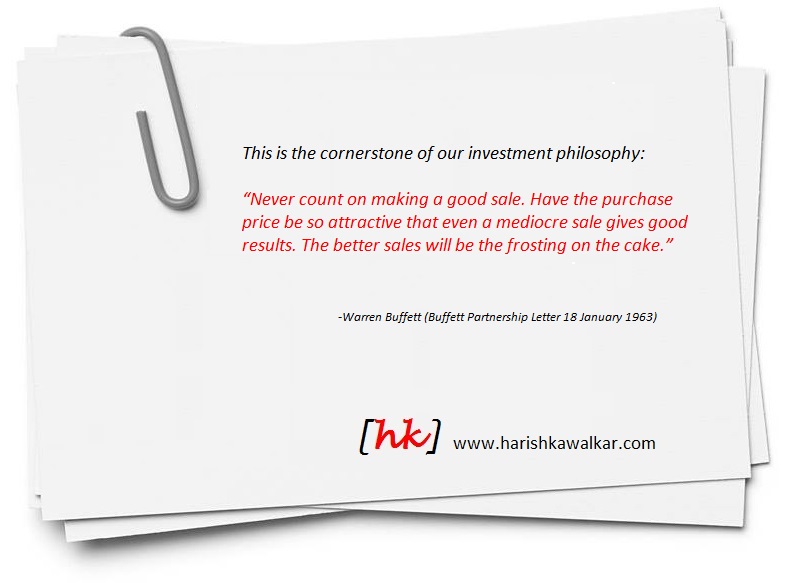

3) By buying assets at a bargain price, we don’t need to pull any rabbits out of a hat to get extremely good percentage gains. This is the cornerstone of our investment philosophy:

“Never count on making a good sale. Have the purchase price be so attractive that even a mediocre sale gives good results. The better sales will be the frosting on the cake.”

Dempster received unsecured term loan of $ 1250000, these funds with funds freed after selling of assets, will be more than the $35 per share, which was the Buffett’s purchase price per share. The present valuation of $16 per share in the manufacturing operation and $35 in security operation.

We, of course, are devoted to compounding the $16 in manufacturing at an attractive rate and believe we have some good ideas as to how to accomplish this. While this will be easy if the business as presently conducted earns money, we have some promising ideas even if it shouldn’t.

It should be pointed out that Dempster last year was 100% an asset conversion problem and therefore, completely unaffected by the stock market and tremendously affected by our success with the assets. In 1963, the manufacturing assets will still be important, but from a valuation standpoint it will behave considerably more like a general since we will have a large portion of its money invested in generals pretty much identical with those in Buffett Partnership, Ltd. For tax reasons, we will probably not put workouts in Dempster. Therefore, if the Dow should drop substantially, it would have a significant effect on the Dempster valuation. Likewise, Dempster would benefit this year from an advancing Dow which would not have been the case most of last year.

There is one final point of real significance for Buffett Partnership, Ltd. We now have a relationship with an operating man which could be of great benefit in future control situations. Harry had never thought of running an implement company six days before he took over. He is mobile, hardworking and carries out policies once they are set. He likes to get paid well for doing well, and I like dealing with someone who is not trying to figure how to get the fixtures in the executive washroom gold-plated.

Harry and I like each other, and his relationship with Buffett Partnership, Ltd. should be profitable for all of us.

The Question of Conservatism

You can read this section in 1961 letter click here

The Usual Prediction

You can read this section in 1962 letter click here

Buffett explains great points.

Buffett explains the ground rules, these are not the partnership rules but these are the Investment ground rules.Buffett has entire networth invested in Buffett Partnership Ltd (Skin in the game)

10% margin over the Dow will be great achievement

Don’t Expect the same performance year on year (Hindsight Bias)

Buffett compounding rate was 21.1%

Buffett explains the joys of compounding, explain the example of Columbus

Compounding happens due to long period of time and the rate at which compounding works

The important point to note is that relatively small difference in rate yields great sums over a long period of time.

Three methods of operation i.e. Generals, Workouts and Control

Dempster Mill turnaround with the help of Harry Bottle

Purchasing price is important than selling price

This is the cornerstone of our investment philosophy:

“Never count on making a good sale. Have the purchase price be so attractive that even a mediocre sale gives good results. The better sales will be the frosting on the cake.”

(Disclaimer: All figures and data used from Buffett Partnership Letter (Dated, 18 January 1963), all are my opinions, and this is for educational purpose only. I am not genius or clever to understand all things, I may be wrong in interpreting the data and letter, take your decision on your own)

To Your Success with Lot of Love!

Harish S Kawalkar

PS: Ask yourself, who is my most valuable client? If you find the answer, then its right place for you..!!!!! The best letter on the Internet Today, Don’t miss, reading, be ready to learn multidisciplinary thinking and become more successful. Sign up! For http://eepurl.com/E2poT (It’s Free)

PPS: If you would like to know the Secrets of Legendry Investors, Buy my EBook

WHAT WORKS IN INVESTING, THE SECRETS OF LEGENDRY INVESTORS

Copyright © 2017 All rights reserved